[ad_1]

Allan Akins/iStock through Getty Pictures

The short-term fairness threat premium is again to ranges not seen since earlier than the Monetary Disaster and money is piling into bonds, BofA Securities says.

The U.S. 2-year Treasury yield is now 280 foundation factors larger than the S&P 500 dividend yield (SDY), the widest unfold since 2007 and buyers are “flooding to short-duration bonds (NASDAQ:SHY),” strategist Michael Hartnett wrote within the weekly Circulation Present observe.

The chance to equities is that this continues through rotation from shares (NYSEARCA:SPY) (QQQ) (DIA) (IWM) (IWB),” Hartnett mentioned.

As well as, “US business financial institution deposits (are) down file $360bn since April ’22 peak ($18.1tn),” with rotation to T-bills and different debt a giant issue,” Hartnett added.

However it’s essential to notice that the “final nice disorderly drop in financial institution deposits was 1994 (Orange County, Mexico peso credit score occasions),” he mentioned.

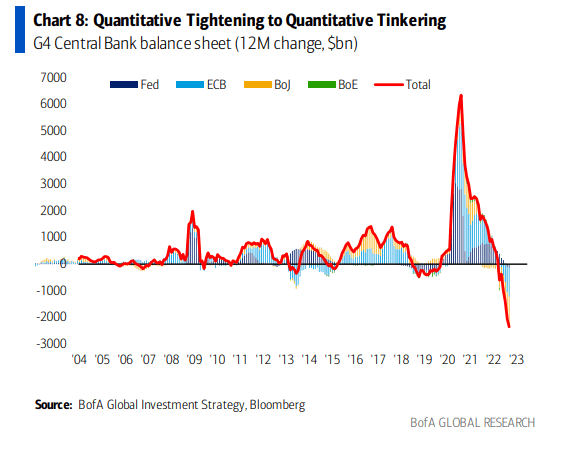

A bullish inventory setting could possibly be discovered, although, if there’s a excessive within the U.S. greenback (DXY) (USDOLLAR) (UUP) that signifies a shift from quantitative tightening to quantitative tinkering. That is the place central banks develop into “fearful of market penalties of liquidity withdrawal” like these seen within the U.Ok., Hartnett mentioned.

The three trades

Hartnett outlined three commerce situations:

- Fundamental Commerce – Lengthy T-bills and short-dated Treasuries on massive yield, hedging for a recession and credit score occasion.

- Ache Commerce – New highs in spreads and a flush within the S&P (SP500) to the pre-COVID excessive of three,333 because the bear rally in threat turns into “too consensus.”

- Useless Commerce – Lengthy U.S. greenback and Massive Tech within the U.S, Massive Luxurious (LUXE) in Europe.

“We’re bearish regardless of ubiquitous bear sentiment; inflation shock, charges shock ongoing + recession shock & credit score shock beginning; new highs in yields, spreads, low in shares coming.”

Might the 10-year yield topping 4.5% carry concerning the sought-after washout in sentiment?

Source link